BDSwiss App

Download & start trading

PREVIOUS WEEK’S EVENTS (Week 11 – 15.03.2024)

Announcements:

U.S. Economy

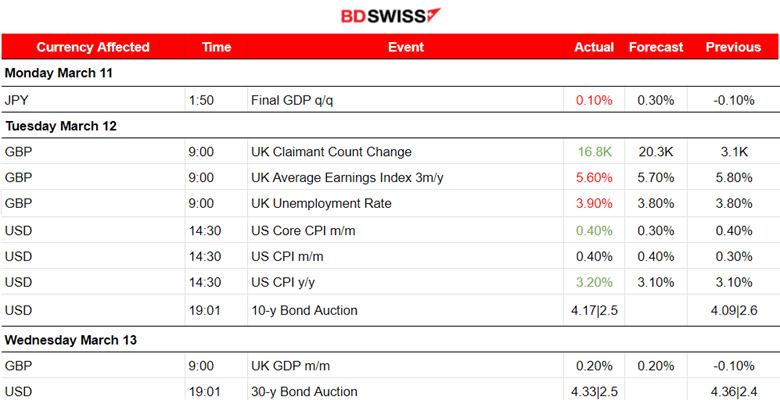

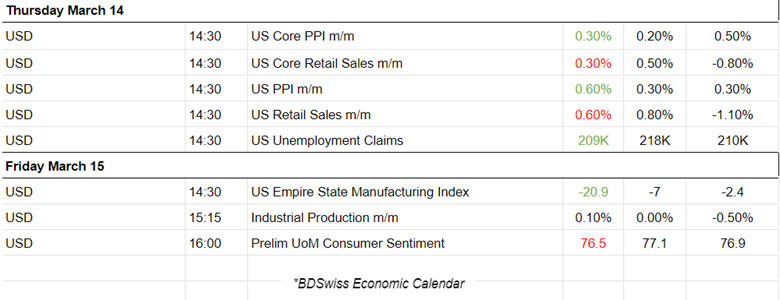

According to the reports for PPI and Retail Sales in the U.S., Producer prices experienced a jump and retail sales were reported to grow. The U.S. stocks dropped, chipmaker stocks extending losses for a second day as expectations that the Federal Reserve might wait longer than expected to cut interest rates are formed.

The Fed is expected to leave rates unchanged at its policy meeting next week amid hot inflation readings for the last two months now.

U.S. consumer sentiment and inflation expectations were a little bit changed in March. However, it is notable that the overall Consumer Sentiment Index came down to 76.5 this month, compared to a final reading of 76.9 in February, according to the University of Michigan’s preliminary reading.

The survey’s reading of one-year inflation expectations was unchanged at 3.0% in March. The survey’s five-year inflation outlook held steady at 2.9% for the fourth straight month.

United Kingdom Economy

Unemployment-related benefits (Claimant Count) are higher (for February 2024 period) than previous and with lower average earnings reported. The unemployment rate for the U.K. rose to 3.9% from 3.8 %. The labour market slowed sharply in February as recruitment firms reported the biggest drop in demand for staff from employers since the coronavirus lockdown of early 2021.

Starting salaries for permanent staff rose at the weakest rate since March 2021. Expected wage growth for companies in the BoE survey was unchanged at 5.2% for the coming year on the three-month moving average basis which the BoE focused on, although on a single-month basis, it dropped to 4.9%, the lowest since May 2022.

According to the Gross Domestic Product (GDP) report, Britain’s economy returned to growth in January after entering a shallow recession in the second half of 2023. GDP grew by 0.2% month-on-month, boosted by a rebound in retailing and house-building – after a fall of 0.1% in December as expected.

______________________________________________________________________

Inflation

U.S.

According to the U.S. inflation report, consumer prices increased solidly in February amid higher costs for gasoline and shelter, figures that could delay an anticipated June interest rate cut from the Federal Reserve.

The consumer price index (CPI) rose 0.4% last month after climbing 0.3% in January. A little hotter than expected, particularly core inflation which is still significantly above the 2% target. If we consider Powell’s speech last week, he said he’s data-driven and since higher prices are not really coming down that much the return to 2% inflation doesn’t seem to be coming any time soon, there is too much uncertainty on when cuts will take place.

______________________________________________________________________

Sources:

https://www.reuters.com/world/uk/uk-economy-grows-by-02-january-2024-03-13

_____________________________________________________________________________________________

Currency Markets Impact – Past Releases (Week 11 – 15.03.2024)

Server Time / Timezone EEST (UTC+02:00)

_____________________________________________________________________________________________

FOREX MARKETS MONITOR

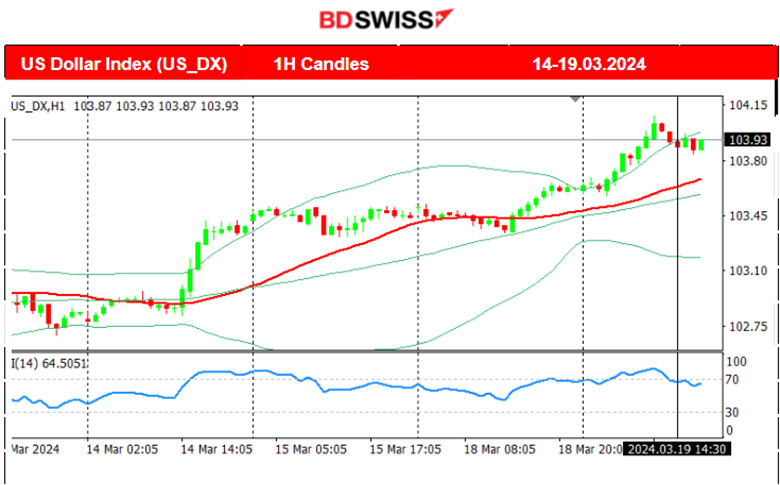

Dollar Index (US_DX)

The U.S. dollar index moved to the upside significantly with the release of higher-than-expected inflation figures last week. On the 12th of March, the CPI figures were released while the PPI figures were released on the 14th of March. Then the USD started to gain strength moving higher and higher on a short-term upward trend. The market responded as expected since the Fed stated that the decisions in regard to cuts will be economic data dependent.

EURUSD

EURUSD

The pair moved to the downside due to USD;s high strengthening overall. The path was volatile since occasionally the EUR was experiencing appreciation. However, the volumes are not enough to beat USD appreciation against the EUR volumes. The short-term weekly downtrend is apparent.

_____________________________________________________________________________________________

_____________________________________________________________________________________________

CRYPTO MARKETS MONITOR

BTCUSD

Bitcoin moved lower and lower after reaching the peak at 74K USD on the 14th of March. Big outflows move bitcoin’s price to the downside and that is quite apparent.

The price is currently below 64K USD as it retraced almost to the 61.8 fibo level of the Daily Chart starting the movement upwards from 42K which is the 0 Fibo level. 100 Fibo is 74K USD and 61.8 Fibo is near the 63K USD level.

_____________________________________________________________________________________________

_____________________________________________________________________________________________

NEXT WEEK’S EVENTS (18 – 22.03.2024)

Coming up:

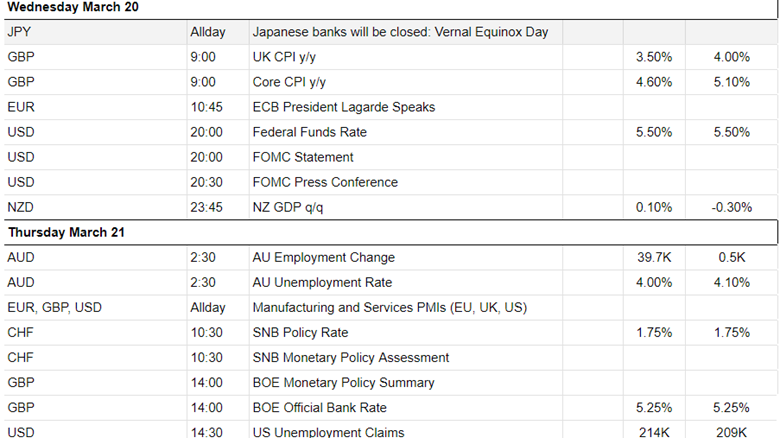

The Reserve Bank of Australia (RBA) kept rates steady, officially setting an end to hikes.

Bank of Japan (BOJ) Interest rate policy change has already taken place, shaking the markets. JPY initial weakening. USD appreciated.

Canada’s and the U.K.’s Inflation is next to be released.

The FOMC takes place on the 20th of March with the market expecting no change in interest rates.

The Swiss National Bank (SNB) and the Bank of England (BOE) decide on rates next.

Currency Markets Impact:

Currency Markets Impact:

_____________________________________________________________________________________________

COMMODITIES MARKETS MONITOR

U.S. Crude Oil

On the 13th of March, Crude started to see a rise in price that was kept steady for two consecutive days causing the price to reach a peak near 81 USD /b. Retracement followed, back to near 80 USD/b. On the 14th of March, the price continued to show that the trend was likely to continue upward and after reaching the resistance near 81 USD/b it retraced to the 30-period MA. On the 18th of March, the price reached the next resistance at near 82.5 USD/b before retracing again to the MA. A clear short-term uptrend that might end soon as the RSI shows a slowdown.

Gold (XAUUSD)

Gold (XAUUSD)

Gold will be pushed to the downside only if the Fed hints that there will be cut delays, following the higher-than-expected inflation. Gold remained high as it moved to the upside on the 13th of March. The U.S. dollar weakened and Gold moved to the upside crossing the 30-period MA on its way up. A triangle formation was visible as volatility is lowering for Gold. Despite recent strong USD appreciation, Gold remains high and sees resilience for the downside.

_____________________________________________________________________________________________

_____________________________________________________________________________________________

EQUITY MARKETS MONITOR

NAS100 (NDX)

Price Movement

On the 13th of March, the upward wedge was broken to the downside and the index dropped until the support at near 18,040 USD, moving below the 30-period MA on its way down. With the dollar appreciating further the drop continued on the 14th of March reaching the support near 17,950 USD before retracing to MA again. The 15th March noted the confirmation of a downfall for U.S. indices as fears that there will be a cut delay grew, with borrowing costs to remain high in the future, and amid the U.S. dollar strengthening. On the 18th of March though, the index moved rapidly upwards and then retraced again to the MA. Currently, the lows are about to be tested again, however a sideways movement is more probable before the FOMC statement takes place tomorrow.

______________________________________________________________

Marios Kyriakou

Marios Kyriakou

Posted on 23 April, 2024 at 12:32 GMT

Posted on 15 April, 2024 at 17:19 GMT

Posted on 08 April, 2024 at 16:57 GMT